After the last few weeks’ market turbulence triggered by escalating tariff headlines, April 2 -28, 2025, delivered a textbook bounce—one that Fibonacci traders could spot a mile away. The QQQ, DJIA, and NASDAQ all staged strong retracements, each pulling back close to the 50% from their recent swing highs to the dramatic lows set by the tariff-driven selloff.

A Closer Look at the 50% Retracement

For those who track Fibonacci levels, the 50% retracement is more than just a number—it often signals a crucial moment of decision in market psychology. It’s the point where bulls and bears reassess their convictions. On April 29, all three major indices touched this level in near-perfect unison.

Let’s break it down:

QQQ (Invesco QQQ Trust): After plunging nearly 6% during the tariff turmoil, QQQ bounced back sharply. On 4/29, it retraced exactly 50% of the down move, landing right on the Fibonacci line drawn using AIQ TradingExpert Pro.

DJIA (Dow Jones Industrial Average): The Dow’s recovery was equally telling. It reclaimed 50% of the decline from its January high to the low posted on April 7. Resistance formed precisely at this level, adding credibility to the Fibonacci reading.

NASDAQ Composite: Tech stocks led the rally, and the NASDAQ showed an aggressive bounce. Like the QQQ, it retraced half the loss, with AIQ TradingExpert Pro’s Fibonacci tool providing a clean visual confirmation of market memory at play.

QQQ and DJIA at the 50% retracement

NASDAQ market at 50% retracement

Using AIQ TradingExpert Pro to Catch the Move

At AIQ, we emphasize practical tools that help traders act, not just analyze. The Fibonacci Retracement tool in AIQ TradingExpert Pro offers an intuitive interface for plotting retracement levels from any significant swing high to low—or vice versa. The 38.2%, 50%, and 61.8% levels are automatically calculated and displayed, making it easy to see where price might hesitate or reverse.

What made April 29 especially notable was how cleanly price respected the 50% level across indices. It wasn’t a vague “zone”—it was a laser line, and those who had it on their charts were better prepared to anticipate resistance and manage risk.

What’s Next?

While the 50% retracement is not a guaranteed reversal point, it is often where institutional players test the bounce’s resolve. If price holds below that level, the odds tilt toward a retest of the recent lows. A strong break above it? Then, we could see a move to the 61.8% level or higher.

With markets still on edge from macro headlines, now’s the time to stay sharp. Fibonacci tools like those in AIQ TradingExpert Pro give traders a clear visual framework, especially during volatile, headline-driven price swings.

Final Thoughts

If you’re not already using Fibonacci levels in your trading, April 29 was a perfect demonstration of their relevance. Whether you’re swing trading or managing a portfolio, these retracement zones offer insight into crowd behavior and price structure. It was noteworthy that the SP500 index had progressed further than 50% retracement (55%)

Stay tuned as we monitor whether this 50% level becomes a ceiling—or just another stepping stone on the road to recovery.

One of the most powerful, yet underutilized technical indicators in AIQ TradingExpert Pro toolkit is the MoneyFlow indicator. Unlike traditional volume-based indicators, the AIQ MoneyFlow combines price action with volume to give a more accurate picture of where institutional money may be flowing. It can be beneficial for timing entries—helping traders spot early accumulation phases before price breakouts occur. At its core, the indicator compares up-volume to down-volume, adjusting for price movement. Important signals occur around trends and trend breaks, and non conformations (highs and lows do not agree) and divergences (trends do not agree) with the price action of the ticker.

Take, for example, the recent action in Nvidia (NVDA). In mid-March 2025, the AIQ Money Flow indicator continued to hold up during the significant downturn in price.

Traders who acted on this early shift, using it as confirmation alongside a breakout pattern, could have caught a strong upside move. Traders can fine-tune this signal to fit a range of strategies, from swing trades to longer-term entries.

The key benefit of using AIQ’s Money Flow indicator for entries is its unique blend of volume and price momentum analysis. It can be combined with group/sector analysis and price momentum indicators as a dynamic tool for identifying stocks where the “smart money” might be stepping in. The Money Flow indicator is a must-watch metric for traders looking to upgrade their entry strategies, especially when markets are volatile and traditional signals are slow

In this update, we’re going to discuss the most recent market timing signals from the Expert system within our Trading Expert Pro platform.

On your screen is a daily chart of the Dow Jones Industrial Average with a price phase indicator underneath, displaying Heiken Ashi-mode candles. The green bars indicate an uptrend, red bars show a downtrend, and the bars that are neither green nor red are based on a color study indicating a high market rating. To explain these market ratings: over 400 rules run through an inference engine—a decision tree process where 400 different indicator states are evaluated. When one rule fires, it triggers the evaluation of certain other rules. These decision pathways contribute to a high expert rating, either up or down, which can signal a change in market direction.

The expert rules are based on historical Dow Jones price action and the internals of the New York Stock Exchange, such as new highs, new lows, and advancing/declining issues, evaluated using numerous indicators. Every day, we generate an expert rating. Most ratings are neutral, meaning few or no rules fired. For instance, on June 4th of this year, the rating was neutral. Once the rules’ weighting reaches beyond 95 up or down, it’s a significant level. On the price chart, buy and sell points are indicated for ratings greater than 95. I’ve marked only the first in a batch of signals; subsequent signals reinforce the initial one. For example, a sell signal is marked by a yellow bar indicating a 96 down rating, signifying importance. Each day, an expert rating is shown on the chart. Scrolling forward, you’ll see the numbers change. White bars indicate a 95 or greater up signal, while yellow bars show a 95 or greater down signal.

The charts are annotated with buy and sell signals. When multiple buy signals occur, we focus on the first one, with subsequent signals reinforcing it. The same applies to sell signals. We haven’t updated these market timing signals in a while. Starting back in late February 2024, there was a buy signal on February 22nd, indicating a 95 rating for the upside. The rules contributing to this signal include the advanced decline oscillator turning positive, viewed as bullish in the market. The New York breadth data’s new high/low indicator reversing to the upside also supports this bullish signal. Price action moved up slightly before flattening out, followed by a sell signal. Examining the sell signal rules, volume accumulation percentages decreased, and the stochastic moved below the 80% line, indicating bearish conditions. Buy and sell signals appear consistently, with some leading to short-term gains.

Recently, on June 6th, there was another sell signal, reinforcing a previous one. Rules indicated negative shifts in the advanced decline line and up-down volume oscillator. These strong signals suggest a continued downtrend. The system, tested over 37 years, uses an inference engine decision tree process, providing standardized market analysis.

For a closer look, visit aiqsystems.com and try our service for a month for just $1, including end-of-day data. This system’s consistency over the years speaks for itself. https://aiqeducation.com/1-trial/

Recording of FREE 90-minute AIQ Zoom meet on September 7, 2023.

In this 90-minute session, Steve Hill, CEO of AIQ Systems looked at Market Timing based on Sector Rotation + David Wozniak of TFR will cover a Mid-Year Market Forecast

Please note due to recording issues the first 5 minutes of the session has some external noise.

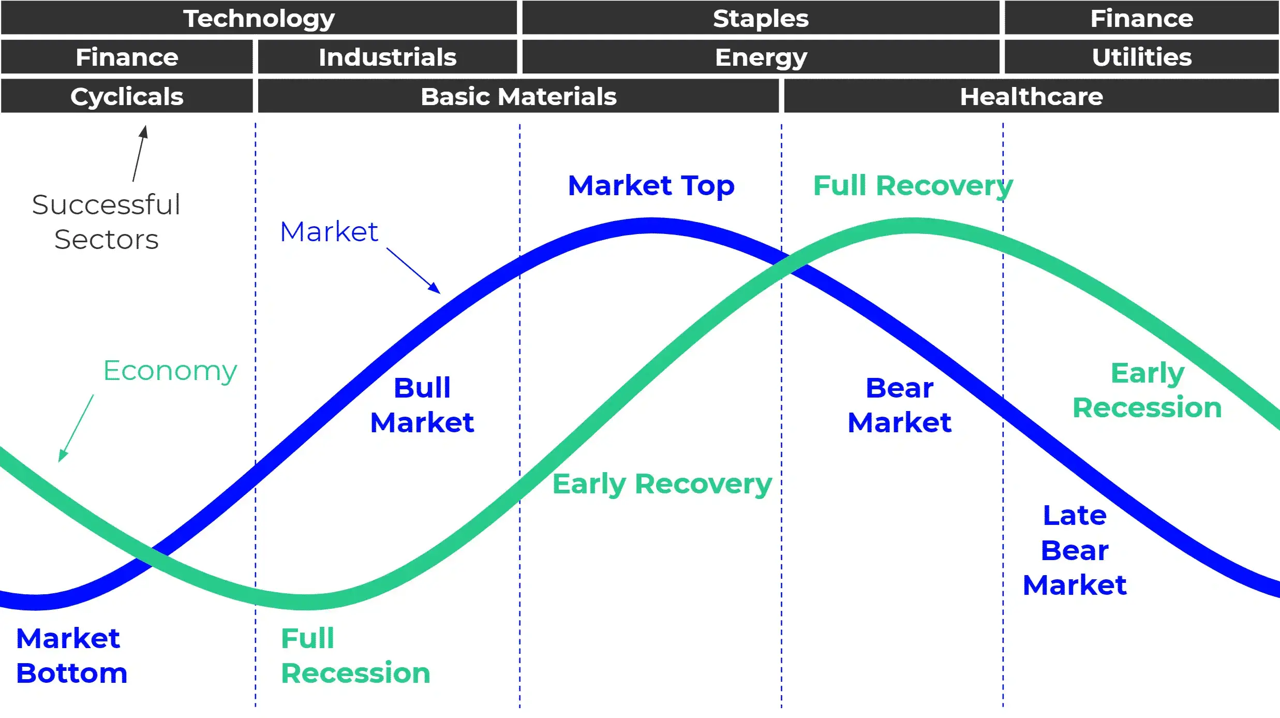

In many ways the markets imitate life. For example, the trend is your friend. You may enjoy your friendship with the trend for an indefinite length of time. But the moment you ignore it – or just simply take it for granted that this friendship is permanent, with no additional effort required on your part – that’s when the trouble starts.

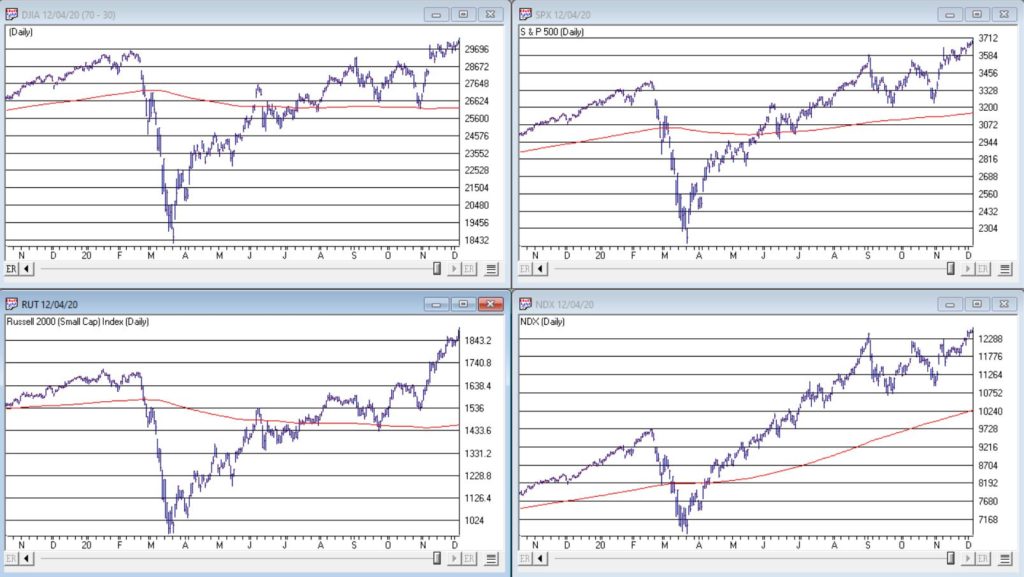

For the stock market right now, the bullish trend is our friend. Figure 1 displays the 4 major indexes all above their respective – and rising – long-term moving averages. This is essentially the definition of a “bull market.”

In addition, a number of indicators that I follow have given bullish signals in the last 1 to 8 months. These often remain bullish for up to a year. So, for the record, with my trusted trend-following, oversold/thrust and seasonal indicators mostly all bullish I really have no choice but to be in the bullish camp.

Not that I am complaining mind you. But like everyone else, I try to keep my eyes open for potential signs of trouble. And of course, there are always some. One of the keys to long-term success in the stock market is determining when is the proper time to actually pay attention to the “scary stuff.” Because scary stuff can be way early or in other cases can turn out to be not that scary at all when you look a little closer.

So, let’s take a closer look at some of the scary stuff.

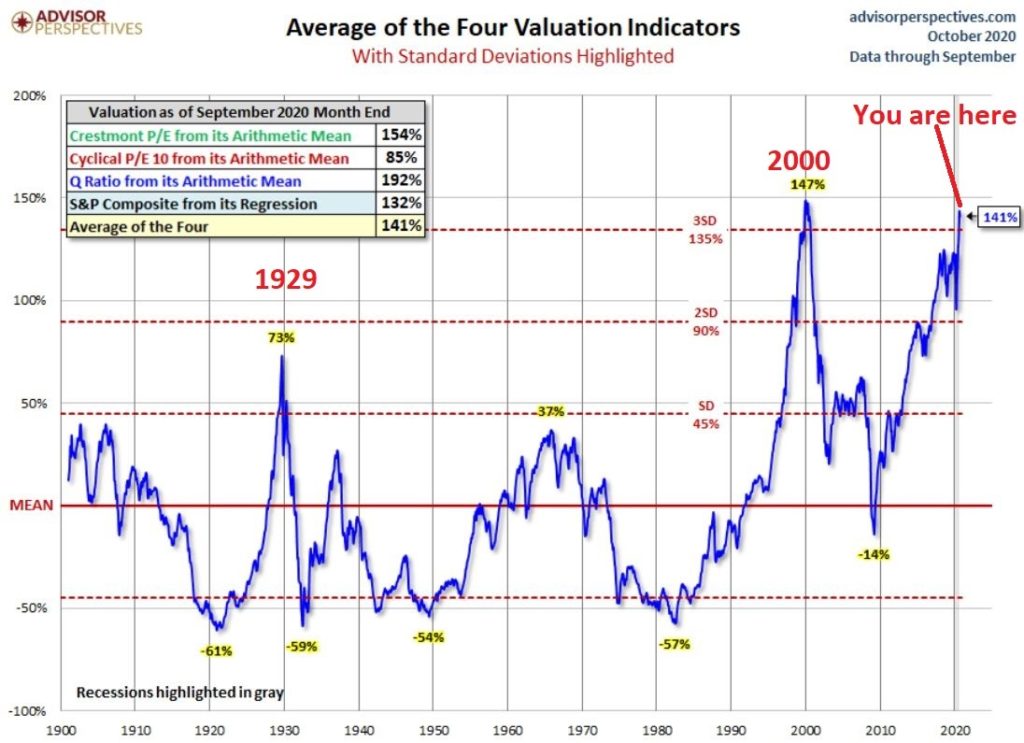

Valuations

Figure 2 displays an aggregate model of four separate measures of valuation. The intent is to gain some perspective as to whether stocks are overvalued, undervalued or somewhere in between.

Clearly the stock market is “overvalued” if looked at from a historical perspective. The only two higher readings preceded the tops in 1929 (the Dow subsequently lost -89% of its value during the Great Depression) and 2000 (the Nasdaq 100 subsequently lost -83% of its value).

Does this one matter? Absolutely. But here is what you need to know:

*Valuation IS NOT a timing indicator. Since breaking out to a new high in 1995 the stock market has spent most of the past 25 years in “overvalued” territory. During this time the Dow Industrials have increased 700%. So, the proper response at the first sign of overvaluation should NOT be “SELL.”

*However, ultimately valuation DOES matter.

Which leads directly to:

Jay’s Trading Maxim #44: If you are walking down the street and you trip and fall that’s one thing. If you are climbing a mountain and you trip and fall that is something else. And if you are gazing at the stars and don’t even realize that you are climbing a mountain and trip and fall – the only applicable phrase is “Look Out Below”.

So, the proper response is this: instead of walking along and staring at the stars, keep a close eye on the terrain directly in front of you. And watch out for cliffs.

Top 5 companies as a % of S&P 500 Index

At times through history certain stocks or groups of stocks catch “lightning in a bottle.” And when they do the advances are spectacular, enriching anyone who gets on board – unless they happen to get on board too late. Figure 3 displays the percentage of the S&P 500 Index market capitalization made up by JUST the 5 largest cap companies in the index at any given point in time.

Figure 3 – Top 5 stocks as a % of S&P 500 Index market cap (Courtesy: www.Bloomberg.com)

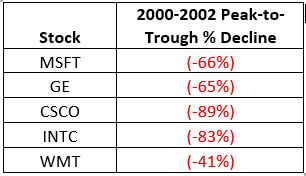

The anecdotal suggestion is pretty obvious. Following the market peak in 2000, the five stocks listed each took a pretty significant whack as shown in Figure 4.

Figure 4 – Top Stocks after the 2000 Peak

Then when we look at how far the line in Figure 3 has soared in 2020 the obvious inference is that the 5 stocks listed for 2020 are due to take a similar hit. And here is where it gets interesting. Are MSFT, AAPL, AMZN, GOOGL and FB due to lose a significant portion of their value in the years directly ahead?

Two thoughts:

*There is no way to know for sure until it happens

*That being said, my own personal option is “yes, of course they are”

But here is where the rubber meets the road: Am I presently playing the bearish side of these stocks? Nope. The trend is still bullish. Conversely, am I keeping a close eye and am I willing to play the bearish side of these stocks? Yup. But not until they – and the overall market – actually starts showing some actual cracks.

One Perspective on AAPL

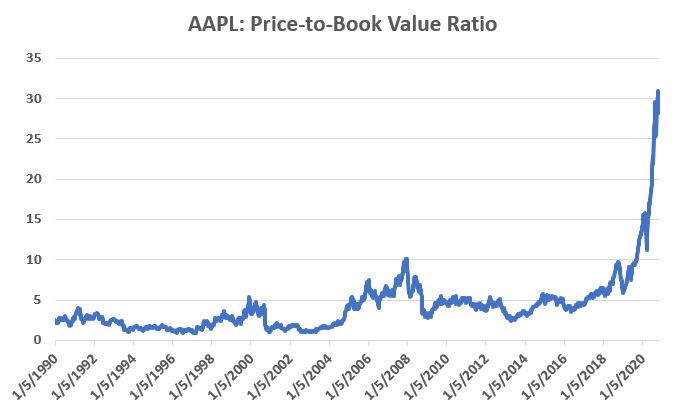

Apple has been a dominant company for many years, since its inception really. Will it continue to be? I certainly would not bet against the ability of the company to innovate and grow its earnings and sales in the years ahead. Still timing – as they say – is everything. For what it is worth, Figure 5 displays the price-to-book value ratio for AAPL since January 1990.

Figure 5 – AAPL price-to-book value ratio (Data courtesy of Sentimentrader.com)

Anything jump out at you?

Now one can argue pretty compellingly that price-to-book value is not the way to value a leading technology company. And I probably agree – to a point. But I can’t help but look at Figure 5 and wonder if that point has possibly been exceeded.

Summary

Nothing in this piece is meant to make you “bearish” or feel compelled to sell stocks. For the record, I am still in the bullish camp. But while this information DOES NOT constitute a “call to action”, IT DOES constitute a “call to pay close attention.”

Bottom line: enjoy the bull market but DO NOT fall in love with it.

Jay Kaeppel

Disclaimer: The information, opinions and ideas expressed herein are for informational and educational purposes only and are based on research conducted and presented solely by the author. The information presented represents the views of the author only and does not constitute a complete description of any investment service. In addition, nothing presented herein should be construed as investment advice, as an advertisement or offering of investment advisory services, or as an offer to sell or a solicitation to buy any security. The data presented herein were obtained from various third-party sources. While the data is believed to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Past performance is no guarantee of future results. There is risk of loss in all trading. Back tested performance does not represent actual performance and should not be interpreted as an indication of such performance. Also, back tested performance results have certain inherent limitations and differs from actual performance because it is achieved with the benefit of hindsight.