As usual, you can pretty much see whatever you want to see in today’s stock market. Consider the major indexes in Figure 1, displayed along with their respective 200-day moving averages.

If you “want to” be bullish, you can focus on the fact that all 4 of these major indexes are presently above their respective 200-day moving averages. This essentially defines an “uptrend”; hence you can make a bullish argument.

If you want to be “bearish”, you can focus on the “choppy” nature of the market’s performance and the fact that very little headway has been made since the highs in early 2018. This “looks like” a classic “topping pattern” (i.e., a lot of “churning”), hence you can make a bearish argument.

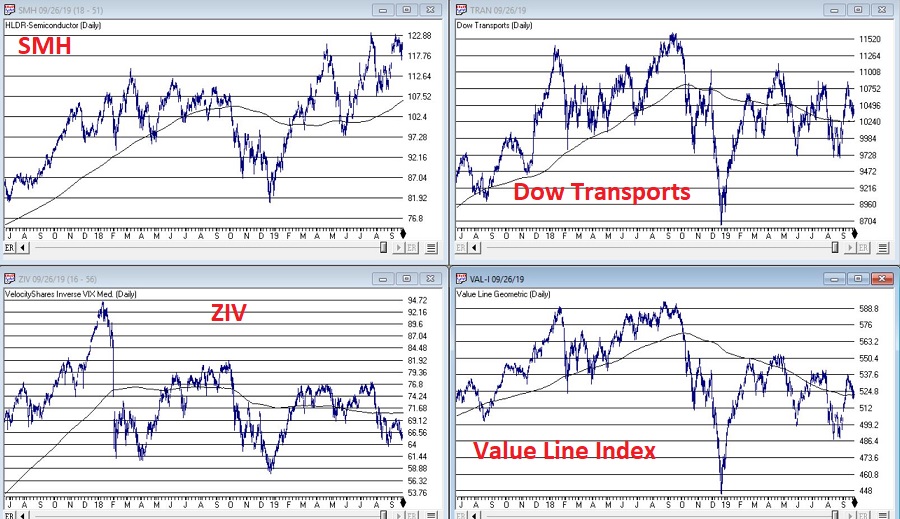

To add more intrigue, consider the 4 “market bellwethers” displayed in Figure 2.

(NOTE: Previously I had Sotheby’s Holdings – ticker BID – as one my bellwethers. As they are being bought out, I have replaced it with the Value Line Arithmetic Index, which has a history of topping and bottoming prior to the major indexes)

The action here is much more mixed and muddled.

*SMH – for any “early warning” sign keep a close eye on the semiconductors. If they breakout to a new high they could lead the overall market higher. If they breakdown from a double top the market will likely be spooked.

*TRAN – The Dow Transports topped out over a year ago and have been flopping around aimlessly in a narrowing range. Not exactly a bullish sign, but deemed OK as long as price holds above the 200-day moving average.

*ZIV – Inverse VIX is presently below it’s 200-day moving average, so this one qualifies as “bearish” at the moment.

*VAL-I – The Value Line Index is comprised of 1,675 stocks and gives each stock equal weight, so is a good measure of the “overall” market. It presently sits right at its 200-day moving average, however – as you can see in Figure 3 – it is presently telling a different story than the S&P 500 Index.

Figure 3 – S&P 500 trending slightly higher, Value Line unweighted index trending lower (Courtesy AIQ TradingExpert)

The Bottom Line

OK, now here is where a skilled market analyst would launch into an argument regarding which side will actually “win”, accompanied by roughly 5 to 50 “compelling charts” that “clearly show” why the analysts’ said opinion was sure to work out correctly. Alas, there is no one here like that.

If the question is, “will the stock market break out to the upside and run to sharply higher new highs or will it break down without breaking out to new highs?”, I sadly must default to my standard answer of, “It beats me.”

Here is what I can tell you though. Instead of relying on “somebody’s opinion or prediction” a much better bet is to formulate and follow an investment plan that spells out:

*What you will (and will not) invest in?

*How much capital you will allocate to each position?

*How much risk you are willing to take with each position?

*What will cause you to exit with a profit?

*What will cause you to exit with a loss?

*Will you have some overarching “trigger” to cause you to reduce overall exposure?

*And so on and so forth

If you have specific answers for the questions above (you DO have specific answers, don’t you?) then the correct thing to do is to go ahead and follow your plan and ignore the myriad prognostications that attempt to sway you one way or the other.

Jay Kaeppel

Disclaimer: The data presented herein were obtained from various third-party sources. While I believe the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. The information, opinions and ideas expressed herein are for informational and educational purposes only and do not constitute and should not be construed as investment advice, an advertisement or offering of investment advisory services, or an offer to sell or a solicitation to buy any security.

Suddenly everyone is once again singing the praises of long-term treasuries. And on the face of it, why not? With interest rates seemingly headed to negative whatever, a pure play on interest rates (with “no credit risk” – which I still find ironic since t-bonds are issued by essentially the most heavily indebted entity in history – the U.S. government) stands to perform pretty darn well.

EDITORS NOTE: We combined Jay's 2 articles on Beating the Bond Market into one article. Later in the article Jay uses AIQ TradingExpert Matchmaker tool to reveal that convertible bonds and high yield corporates have a much higher correlation to the stock market than they do to the long-term treasury.

But is it really the best play?

Long-Term Treasuries vs. “Others”

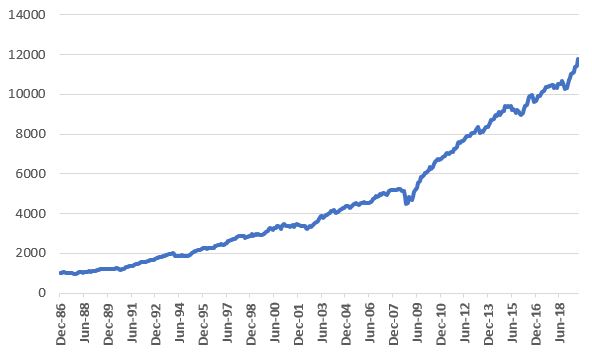

Because a later test will use the Bloomberg Barclays Convertible Bond Index, and because that index starts in 1986 and because I want to compare “apples” to “apples”, Figure 1 displays the growth of $1,000 since 1986 using monthly total return data for the Bloomberg Barclays Treasury Long Index.

Figure 1 – Growth of $1,000 in Long-Term Treasuries (1987-2019)

For the record:

Ave. 12 mo %

+8.2%

Std. Deviation

+9.0%

Max Drawdown

(-15.9%)

$1,000 becomes

$12,583

Figure 2 – Bloomberg Barclays Treasury Long Index (Jan 1987-Jul 2019)

Not bad, apparently – if your focus is return and you don’t mind some volatility and you have no fear of interest rates ever rising again.

A Broader Approach

Now let’s consider an approach that puts 25% into the four bond indexes below and rebalances every Jan. 1:

*Bloomberg Barclay’s Convertible Bond Index

*Bloomberg Barclays High Yield Very Liquid Index

*Bloomberg Barclays Treasury Long Index

*Bloomberg Barclay’s Intermediate Index

Figure 3 displays the growth of this “index” versus buying and holding long-term treasuries.

Figure 3 – Growth of $1,000 invested in 4-Bond Indexes and rebalanced annually; 1987-2019

Ave. 12 mo %

+8.0%

Std. Deviation

+6.8%

Max Drawdown

(-14.8%)

$1,000 becomes

$11,774

Figure 4 – 4-Bond Index Results; 1987-2019

As you can see, the 4-index approach:

*Is less volatile in nature (6.8% standard deviation versus 9.0% for long bonds)

*Had a slightly lower maximum drawdown

*And has generated almost as much gain as long-term treasuries alone (it actually had a slight lead over long-term treasuries prior to the rare +10% spurt in long treasuries in August 2019)

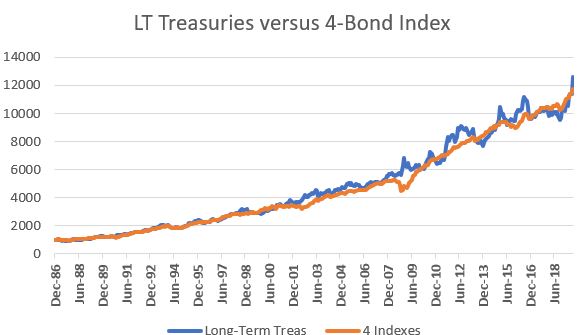

To get a better sense of the comparison, Figure 5 overlays Figures 1 and 3.

Figure 5 – Long Treasuries vs. 4-Bond Index

As you can see in Figure 5, in light of a long-term bull market for bonds, at times long-term treasuries have led and at other times they have trailed our 4-Bond Index. After the huge August 2019 spike for long-term treasuries, they are back in the lead. But for now, the point is that the 4-Bond Index performs roughly as well with a great deal less volatility.

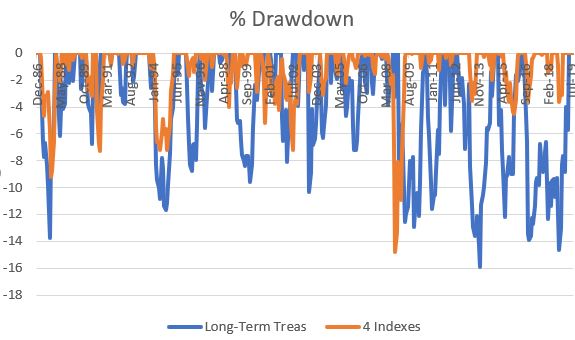

To emphasize this (in a possibly slightly confusing kind of way), Figure 6 shows the drawdowns for long treasuries in blue and drawdowns for the 4-Bond Index in orange. While the orange line did have one severe “spike” down (during the financial panic of 2008), clearly when trouble hits the bond market, long-term treasuries tend to decline more than the 4-Bond Index.

Figure 6 – % Drawdowns for Long-term treasuries (blue) versus 4-Bond Index (orange); 1987-2019

Summary

Long-term treasuries are the “purest interest rate play” available. If rates fall then long-term treasuries will typically outperform most other types of bonds. On the flip side, if interest rates rise long-term treasuries will typically underperform most other types of bonds.

Is this 4-index approach the “be all, end all” of bond investing? Is it even superior to the simpler approach of just holding long-term bonds?

Not necessarily. But there appears to be a better way to use these four indexes – which I will get to below

So, all-in-all the 4-bond index seems like a “nice alternative” to holding long-term treasuries. But the title of these articles says “Beating the Bond Market” and not “Interesting Alternatives that do Just about as Well as Long-Term Treasuries” (which – let’s face it – would NOT be a very compelling title). So, let’s dig a little deeper. In order to dig a little deeper, we must first “go off on a little tangent.”

Bonds versus Stocks

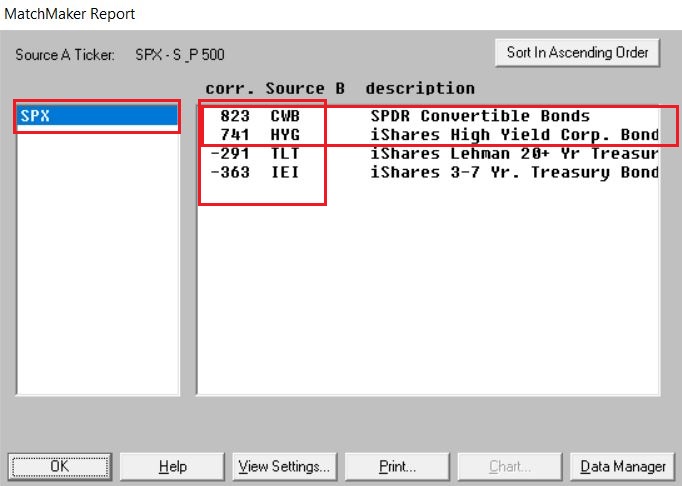

In a nutshell, individual convertible bonds and high yield corporate bonds are tied to the fortunes of the companies that issue them. This also means that as an asset class, their performance is tied to the economy and the business environment in general. If times are tough for corporations it only makes sense that convertible bonds and high yield bonds will also have a tougher time of it. As such it is important to note that convertible bonds and high yield corporates have a much higher correlation to the stock market than they do to the long-term treasury.

In Figures 1 and 2 we use the following ETF tickers:

CWB – as a proxy for convertible bonds

HYG – As a proxy for high-yield corporates

TLT – As a proxy for long-term treasuries

IEI – As a proxy for short-term treasuries

SPX – As a proxy for the overall stock market

BND – As a proxy for the overall bond market

As you can see in Figure 1, convertible bonds (CWB) and high-yield corporates (HYG) have a much higher correlation to the stock market (SPX) than to the bond market (BND).

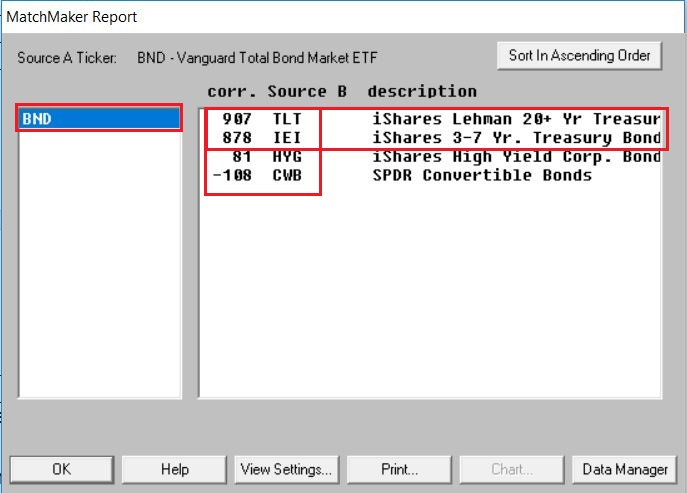

As you can see in Figure 2, long-term treasuries (TLT) and intermediate-term treasuries (IEI) have a much higher correlation to the bond market (BND) than to the stock market (SPX).

Figure 2 – 4-Bond Index Components correlation to Vanguard Total Bond Market ETF (Courtesy AIQ TradingExpert)

A Slight Detour

Figure 3 displays the cumulative price change for the S&P 500 Index during the months of November through April starting in 1949 (+8,881%)

Figure 3 – Cumulative % price gain for S&P 500 Index during November through April (+8,881%); 1949-2019

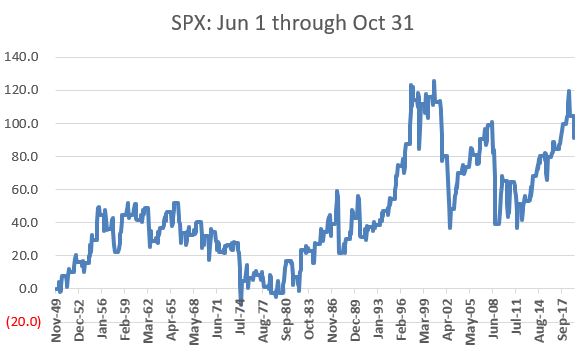

Figure 4 displays the cumulative price change for the S&P 500 Index during the months of June through October starting in 1949 (+91%)

Figure 4 – Cumulative % price gain for S&P 500 Index during June through October (+91%); 1949-2019

The Theory: Parts 1 and 2

Part 1: The stock market performs better during November through April than during May through October

Part 2: Convertible bonds and high-grade corporate bonds are more highly correlated to stocks than long and intermediate-term treasuries

Therefore, we can hypothesize that over time convertible and high-yield bonds will perform better during November through April and that long and intermediate-term treasuries will perform better during May through October.

Jay’s Seasonal Bond System

During the months of November through April we will hold:

*Bloomberg Barclay’s Convertible Bond Index

*Bloomberg Barclays High Yield Very Liquid Index

During the months of May through October we will hold:

*Bloomberg Barclays Treasury Long Index

*Bloomberg Barclay’s Intermediate Index

(NOTE: While this article constitutes a “hypothetical test” and not a trading recommendation, just to cover the bases, an investor could emulate this strategy by holding tickers CWB and HYG (or ticker JNK) November through April and tickers TLT and IEI May through October.)

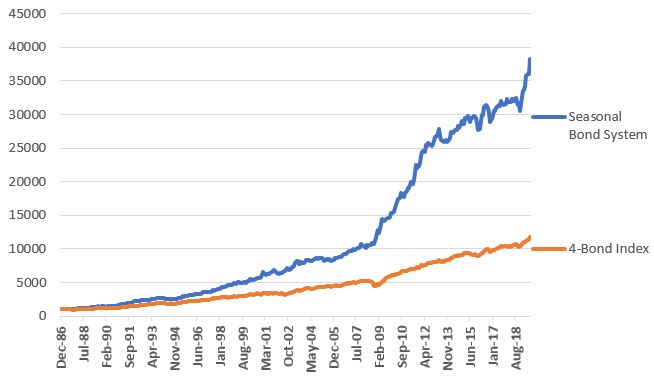

Figure 5 displays the growth of $1,000 invested using this Seasonal System (blue line) versus simply splitting money 25% into each index and then rebalancing on January 1st of each year (orange line).

Figure 5 – Growth of $1,000 invested using Jay’s Seasonal System versus Buying-and-Holding and rebalancing (1986-2019)

Figure 6 displays some comparative performance figures.

Measure

SeasonalSystem

4 Indexes Buy/Hold/Rebalance

Average 12 month % +(-)

+11.9%

+8.0%

Std. Deviation %

8.7%

6.8%

Ave/StdDev

1.37

1.18

Max Drawdown%

(-9.2%)

(-14.8%)

$1,000 becomes

$38,289

$11,774

Figure 6 – Seasonal Strategy versus Buy/Hold/Rebalance

From 12/31/1986 through 8/31/2019 the Seasonal System gained +3,729% versus +1,077% (3.46 times as much) as the buy/hold and rebalance method.

Summary

The Seasonal Bond System has certain unique risks. Most notably if the stock market tanks between November 1 and April 30, this system has no “standard” bond positions to potentially offset some of the stock market related decline that convertible and high yield bonds would likely experience. Likewise, if interest rates rise between April 30 and October 31st, this strategy is almost certain to lose value during that period as it holds only interest-rate sensitive treasuries during that time.

The caveats above aside, the fact remains that over the past 3+ decades this hypothetical portfolio gained almost 3.5 times that of a buy-and-hold approach.

Question: Is this any way to trade the bond market?

Answer: Well, it’s one way….

Jay Kaeppel

Disclaimer: The data presented herein were obtained from various third-party sources. While I believe the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. The information, opinions and ideas expressed herein are for informational and educational purposes only and do not constitute and should not be construed as investment advice, an advertisement or offering of investment advisory services, or an offer to sell or a solicitation to buy any security.

The “barbell” approach to bond investing typically involves buying a long-term bond fund or ETF and a short-term bond fund or ETF. The idea is that the long-term component provides the upside potential while the short-term component dampens overall volatility and “smooths” the equity curve. This article is not intended to examine the relative pros and cons of this approach. The purpose is to consider an alternative for the years ahead.

The Current Situation

Interest rates bottomed out several years ago and rose significantly from mid-2016 into late 2018. Just when everyone (OK, roughly defined as “at least myself”) assumed that “rates were about to establish an uptrend” – rates topped in late 2018 and have fallen off since. Figure 1 displays ticker TYX (the 30-year treasury yield x 10) so you can see for yourself.

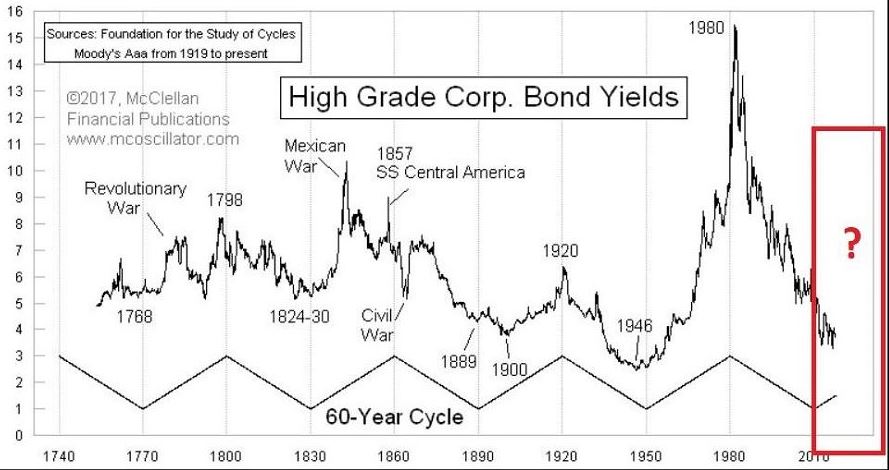

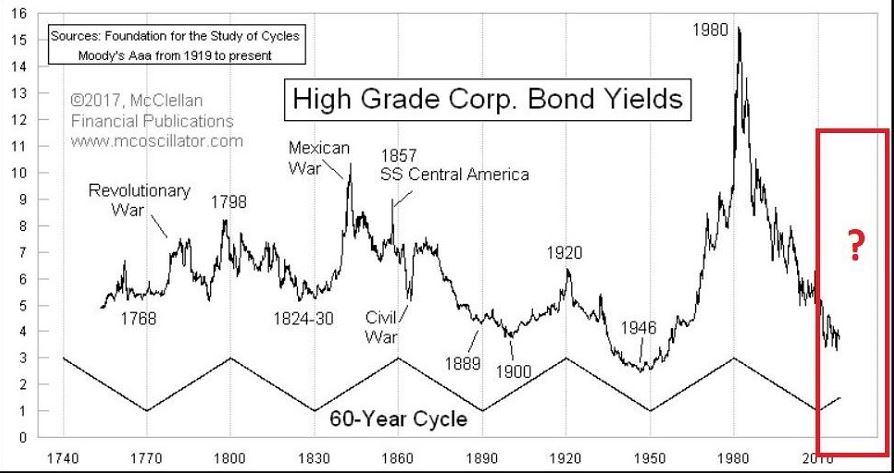

In terms of the bigger picture, rates have showed a historical tendency to move in 30-year waves. If that tendency persists then rates should begin to rise off the lows in recent years in a more meaningful way. See Figure 2.Figure 2 – 60-year wave in interest rates (Courtesy: www.mcoscillator.com)

Will this happen? No one can say for sure. Here is what we do know: If rates decline, long-term treasuries will perform well (as long-term bonds react inversely to the trend in yields) and if rates rise then long-term bond holders stand to get hurt.

So here is an alternative idea for consideration – a bond “barbell” that includes:

*Long-term treasuries (example: ticker VUSTX)

*Floating rate bonds (example: ticker FFRAX)

Just as treasuries rise when rates fall and vice versa, floating rate bonds tend to rise when rates rise and to fall when rates fall, i.e., (and please excuse the use of the following technical terms) when one “zigs” the other “zags”. For the record, VUSTX and FFRAX have a monthly correlation of -0.29, meaning they have an inverse correlation.

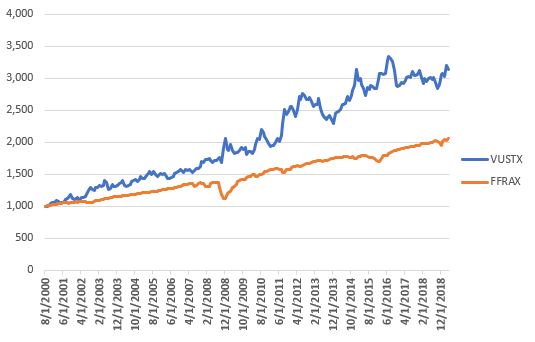

Figure 3 displays the growth of $1,000 invested separately in VUSTX and FFRAX since FFRAX started trading in 2000. As you can see the two funds have “unique” equity curves.

Figure 3 – Growth of $1,00 invested in VUSTX and FFRAX separately

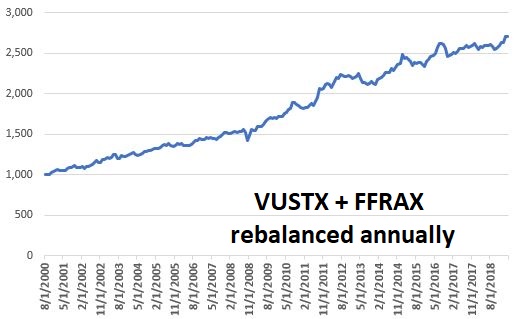

Now let’s assume that every year on December 31st we split the money 50/50 between long-term treasuries and floating rate bonds. This combined equity curve appears in Figure 4.

Figure 4 – Growth of $1,000 50/50 VUSTX/FFRAX; rebalanced annually

Since 2000, long-treasuries have made the most money. This is because interest rates declined significantly for most of that period. If interest rise in the future, long-term treasuries will be expected to perform much more poorly. However, floating rate bonds should prosper in such an environment.

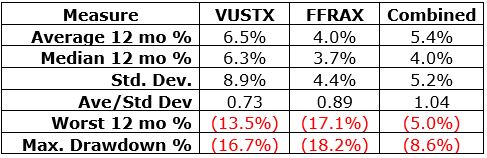

Figure 5 displays some relevant facts and figures.

Figure 5 – Relevant performance Figures

The key things to note in Figure 5 are:

*The worst 12-month period for VUSTX was -13.5% and the worst 12-month period for FFRAX was -17.1%. However, when the two funds are traded together the worst 12-month period was just -5.0%.

*The maximum drawdown for VUSTX was -16.7% and the maximum drawdown for FFRAX was -18.2%. However, when the two funds are traded together the worst 12-month period was just -8.6%.

Summary

The “portfolio” discussed herein is NOT a recommendation, it is merely “food for thought”. If nothing else, combining two sectors of the “bond world” that are very different (one reacts well to falling rates and the other reacts well to rising rates) certainly appears to reduce the overall volatility.

My opinion is that interest rates will rise in the years ahead and that long-term bonds are a dangerous place to be. While my default belief is that investors should avoid long-term bonds during a rising rate environment, the test conducted here suggests that there might be ways for holders of long-term bonds to mitigate some of their interest rate risk without selling their long-term bonds.

Like I said, food for thought.

Jay Kaeppel

Disclaimer: The data presented herein were obtained from various third-party sources. While I believe the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. The information, opinions and ideas expressed herein are for informational and educational purposes only and do not constitute and should not be construed as investment advice, an advertisement or offering of investment advisory services, or an offer to sell or a solicitation to buy any security.

2018 witnessed something of a “fake out” in the bond market. After bottoming out in mid-2016 interest rates finally started to “breakout” to new multi-year highs in mid to late 2018. Then just as suddenly, rates dropped back down.

Figure 1 displays the tendency of interest rates to move in 60-year waves – 30 years up, 30 years down. The history in this chart suggests that the next major move in interest rates should be higher.Figure 1 – 60-year wave in interest rates (Courtesy: www.mcoscillator.com)

A Way to Track the Long-Term Trend in Rates

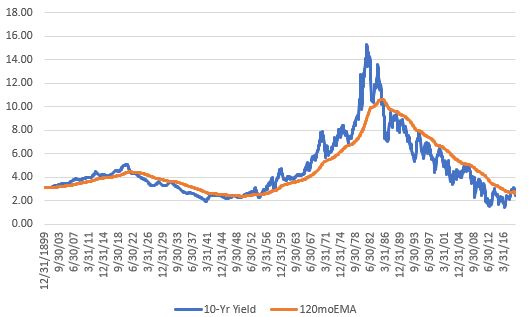

Ticker TNX is an index that tracks the yield on 10-year treasury notes (x10). Figure 2 displays this index with a 120-month exponential moving average overlaid. Think of it essentially as a smoothed 10-year average.

Figure 2 – Ticker TNX with 120-month EMA (Courtesy AIQ TradingExpert)

Interpretation is pretty darn simple. If the month-end value for TNX is:

*Above the 120mo EMA then the trend in rates is UP (i.e., bearish for bonds)

*Below the 120mo EMA then the trend in rates is DOWN (i.e., bullish for bonds)

Figure 3 displays 10-year yields since 1900 with the 120mo EMA overlaid. As you can see, rates tend to move in long-term waves.

Figure 3 – 10-year yield since 1900 with 120-month exponential moving average

Two key things to note:

*This simple measure does a good job of identifying the major trend in interest rates

*It will NEVER pick the top or bottom in rates AND it WILL get whipsawed from time to time (ala 2018).

*Rates were in a continuous uptrend from 1950 to mid-1985 and were in a downtrend form 1985 until the 2018 whipsaw.

*As you can see in Figure 2, it would not take much of a rise in rates to flip the indicator back to an “uptrend”.

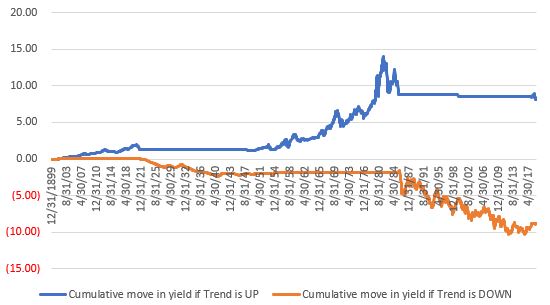

With those thoughts in mind, Figure 4 displays the cumulative up or down movement in 10-year yields when, a) rates are in an uptrend (blue) versus when rates are in a downtrend (orange).

Figure 4 – Cumulative move in 10-year yields if interest rate trend is UP (blue) or DOWN (orange)

You can see the large rise in rates from the 1950’s into the 1980’s in the blue line as well as the long-term decline in rates since that time in the orange line. You can also see the recent whipsaw at the far right of the blue line.

Summary

Where do rates go from here? It beats me. As long as the 10-year yield holds below its long-term average I for one will give the bond bull the benefit of the doubt. But when the day comes that 10-year yields move decisively above their long-term average it will be essential for bond investors to alter their thinking from the mindset of the past 30+ years, as in that environment, long-term bonds will be a difficult place to be.

And that won’t be easy, as old habits die hard.

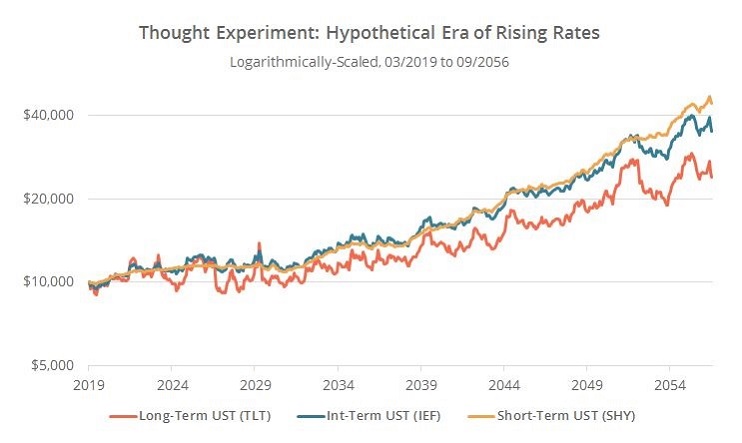

Figure 5 is from this article from BetterBuyandHold.com and displays the project returns for short, intermediate and long term bonds if rates were to reverse the decline in rates since 1982.Figure 5 – Projected total return for short, intermediate and long-term treasuries if rates reverse decline in rate of past 30+ years (Courtesy: BetterBuyandHold.com)

When rates finally do establish a new rising trend, short-tern and intermediate term bonds will be the place to be. When that day will come is anyone’s guess. But the 10-year yield/120mo EMA method at least we have an objective way to identify the trend shortly after the fact.

Jay Kaeppel

Disclaimer: The data presented herein were obtained from various third-party sources. While I believe the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. The information, opinions and ideas expressed herein are for informational and educational purposes only and do not constitute and should not be construed as investment advice, an advertisement or offering of investment advisory services, or an offer to sell or a solicitation to buy any security.

Sometimes it’s good to go back to the basics. So here goes.

Trading success comes from a “reality based” approach. It is NOT about “all the money I am going to make!” It IS about “formulating a plan” (see the questions below) AND “doing the right thing over and over and over again” (no matter how uncomfortable or unsexy those “things” may be).

Steps to Trading Success

Trading success comes from:

A) Having answers to the questions below

B) Remembering the answers through all of the inevitable ups and downs

What vehicles will you trade?

Will it be stocks, ETFs, mutual funds, futures, options, or something else? If you plan to trade futures or options understand that you will need a different account and/or approval from your brokerage firm. Likewise, note that you will need to learn about the unique quirks of futures and options BEFORE you start trading.

How much money will you commit to your trading account?

Whatever that amount is be sure to put the entire amount into your account. DO NOT make the mistake of saying “I only have x$’s but I am going to trade it as if it were y$’s. One good drawdown and you will pull the plug.

How much money will you commit to a single trade/position?

We are NOT talking here about how much of a loss you are willing to endure. We are simply talking about how much you will omit to the enter the trade. If you put 10% of your capital into a given stock or ETF that doesn’t mean you are going to risk the entire amount. This question has more to do with determining how diversified you will be.

How much money will you risk on a given trade/position?

Think in terms of percentages. I will risk 1%, 2%, 5%, 10%, whatever. There is no magic, or correct, number. But think of it this way – “if I experience 5 consecutive losing trades how much will my account be down?” If you can’t handle that number then you need to reduce your risk per trade.

How many different positions will I hold at one time? What is my maximum?

Buying and holding a portfolio stocks is different than actively trading. For active traders, holding a lot of positions at one time can be taxing – much more so than you might expect going in. Don’t learn this lesson the hard way.

Do you understand the mechanics of entering trading orders?

The vast majority of trading orders are placed on-line. Each brokerage firm has their own websites/platforms and each has their unique characteristics. “Paper trading” an be a disaster if you come away thinking you “have the touch” when it comes to making money. However, when it comes to learning the in’s and out’s of order placement BEFORE you actually start trading, it an be invaluable.

(Think of trading as sky diving and paper trading as watching virtual sky diving on your laptop. You get the idea, but the actual experience is significantly different).

What will cause me to enter a trade?

There are roughly a bazillion and one ways to trigger a “buy signal”. Some are great, some are awful, but the majority are somewhere sort of in the middle. Too many traders spend too much time looking for “that one great method”: of triggering signals. The truth is that if you allocate capital wisely, manage your risk (more to follow) the actual method you use to signal trades is just one more piece of the puzzle – NOT the be all, end all.

How will I enter a trade?

This sounds like the same question as the one above, but it is different. For an active trader, a buy signal may occur but he or she may wait for “the right time” to actually enter the market. For example, if an “oversold” indicator triggers a “buy” signal, a trader may wait until there is some sort of price confirmation (i.e., a high above the previous trading day, a close above a given moving average, etc.) rather than risking “trying to catch a falling safe.”

What will cause me to exit a trade with a loss?

The obvious one is a loss that reaches the maximum amount you are willing to risk per trade as established earlier. But there can be other factors. In some cases, if the criteria that caused you to enter the trade in the first place no longer is valid, it can make sense to “pull the plug” and move on to another opportunity. A simple example: you buy because price moves above a given moving average. Price then drops back below that moving average without reaching your “maximum loss” threshold.

What will cause you to exit a trade with a profit?

This one is easy to take for granted. Too many traders think, “Oh, once I get a decent profit I’ll just go ahead and take it.” But a lot depends on the type of methodology that you are using. If you are using a short-term trading system that looks for short-term “pops” in the market, then it might male sense to think in terms of setting “profit targets” and getting out while the getting is good. On the other hand, if you are using a trend-following method you will likely need to maintain the discipline to “let your profits run” in order to generate the big winning trades that virtually all trend-following methods need in order to offset all of the smaller loses that virtually all trend-following methods experience.

The problem comes when a short-term trader decides to “let it ride” or when a trend follower starts “cutting his or her profit short” by taking small profits.

Different Types of Trading Require a Different Mindset

Putting money into a mutual fund or a portfolio of stocks is far different than trading futures or even options. While you can be “hands on” with funds or stocks it is not necessarily a requirement (I still hold a mutual fund that I bought during the Reagan administration). With futures or options, you MUST be – and must be prepared to be – hands on.

Also, big percentage swings in equity are more a way of life in futures and options. I like options because they give you the ability to risk relatively small amounts of capital on any variety of opportunities – bullish, bearish, neutral, hedging and so forth.

I also like futures, but it does require a different level of emotional and financial commitment than most other forms of trading. Many years ago, I wrote about the following “Litmus Test for Futures Traders”. It goes like this:

To tell if you are prepared emotionally and financially to trade futures doe the following.

1. Got to your bank on a windy day.

2. Withdraw a minimum of $10,000 in cash

3. Go outside and start throwing your money up into the air until it all blows away

4. Go home and get back to your routine like nothing ever happened.

If you can pass this test then you are fully prepared to trade futures. If you cannot pass this test it simply means that you need to go into it with your eyes wide open regarding the potential risks (with the knowledge that something similar to what was just described can happen at any time).

Summary

In a perfect world a trader will have well thought out and detailed answers to all of the questions posed above BEFORE they risk their first dollar.

Jay Kaeppel

Disclaimer: The data presented herein were obtained from various third-party sources. While I believe the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. The information, opinions and ideas expressed herein are for informational and educational purposes only and do not constitute and should not be construed as investment advice, an advertisement or offering of investment advisory services,