ETF text with businessman on dark vintage background

If you missed this AIQ Zoom event, don’t worry, the recording is now available from the link at the end of this post. (FYI it expires on April 13th).

In this 90-minute session, Steve Hill, CEO of AIQ Systems built a list of Direxion ETFs to trade everything and ran it through analytical tools. In the second half David Wozniak, CMT covered supply and demand by Incorporating Point & Figure Charts.

Steve also created data files and list files for the ETFS. These are zipped and available below

ETF data files are here – unzip to your /wintes32/tdata folder. Then go to Data Manager, Utilities, Rebuild Master Ticker List.

ETF List files are here – unzip these files to your /wintes32 folder.

The importable AIQ EDS file based on John Ehlers’ article in the March 2023 issue of Stocks & Commodities, “Every Little Bit Helps,” can be obtained on request via rdencpa@gmail.com. John notes ‘It’s simple but makes a noticeable improvement: You can reduce noise in the data by using an average of the open and close instead of using only the closing price.’ The code is also available below.

!Every Little Bit Helps !Author: John F. Ehlers, TASC Mar 2023 !Coded by: Richard Denning, 1/12/2023

!Data Sampling Test !(c) John Ehlers 2022

!INPUTS: W1 is 14. !Wilder RSI length W2 is 14. !Ehlers RSI length

!RSI Wilder code: U is [close]-val([close],1). D is val([close],1)-[close]. L1 is 2 * W1 – 1. AvgU is ExpAvg(iff(U>0,U,0),L1). AvgD is ExpAvg(iff(D>=0,D,0),L1). RSIwilder is 100-(100/(1+(AvgU/AvgD))).

!Ehlers RSI code: OCavg is ([open] + [close])/2. Uoc is OCavg-valresult(OCavg,1). Doc is valresult(OCavg,1)-OCavg. L2 is 2 * W2 – 1. AvgU2 is ExpAvg(iff(Uoc>0,Uoc,0),L2). AvgD2 is ExpAvg(iff(Doc>=0,Doc,0),L2). RSIoc is 100-(100/(1+(AvgU2/AvgD2))).

!CTest is RSIwilder. !OCTest is RSIoc.

BuyRSIwilder if RSIwilder < 20 and valrule(RSIwilder >= 20,1). ExitRSIwilder if RSIwilder > 80 or {Position days}>=20.

BuyRSIoc if RSIoc < 20 and valrule(RSIoc >= 20,1). ExitRSIoc if RSIoc > 80 or {Position days}>=20.

Code for the author’s indicators are set up in the AIQ EDS code file. Figure 7 shows the EDS module backtest results using the RSI original indicator. Figure 8 shows the EDS module backtest results using the modified version of the RSI indicator over a 10-year period using NASDAQ 100 stocks. The comparison suggests that some of the metrics improve using the modified version and a few are worse.

The system rules are:

Buy when the RSI crosses down below 20

Sell when the RSI crosses above 80 or after 20 trading days

FIGURE 7: AIQ. This shows example backtest results for classic RSI trading system rules, based on closing data, over a 10-year period using NASDAQ 100 stocks. FIGURE 8: AIQ. This shows example backtest results for the RSI trading system rules, this time based on data that averages the open and close instead of using just the closing price data, over a 10-year period using NASDAQ 100 stocks.

This may save to a download folder on your system. We suggest you move it to the path C:/wintes32/EDS strategies/Chart Pattern Strategies folder.

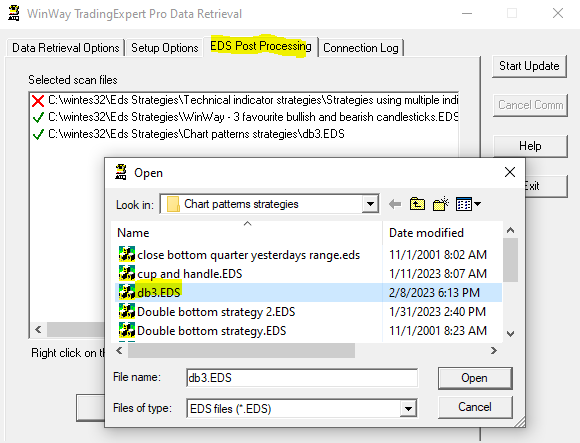

To run this strategy automatically after your nightly download of data

– Open Data Retrieval, and select the EDS Post Processing tab. – Select add, and in the Open, Look in C:/wintes32/EDS strategies/Chart Pattern Strategies folder for db3.EDS – Select Open and the strategy will run every night for you.

In her article in the December 2022 issue of Stocks and Commodities, “Short-Term Continuation And Reversal Signals,” Barbara Star describes modifications to the classic directional movement indicator (DMI) and commodity channel index (CCI) that can aid in more easily identifying price reversals and continuations in a trend. Traditionally, the DMI is comprised of two lines: a positive line (+DI) and negative line (−DI).

In her article, Star creates a DMI oscillator by subtracting −DI from +DI. Historically, the DMI uses a default length of 14. In the article, this has been shortened to 10. The CCI has also been adjusted in the article to use a length of 13 instead of the usual 14 or 20. The oscillator is setup using an AIQ Color Study

The importable AIQ EDS file can be obtained on request via email to info@TradersEdgeSystems.com. The code is also shown here:

! Short-Term Continuation And Reversal Signals ! Author: Barbara Star, TASC Dec 2022 ! Coded by: Richard Denning, 10/21/2022 C is [close]. H is [high]. L is [low]. H1 is valresult(H,1). H2 is valresult(H,2). L1 is valresult(L,1). L2 is valresult(L,2). GreenDMI if [DirMov] > 0. RedDMI if [DirMov] < 0. StartOfDownTrend if C < simpleavg(C,18) and [DirMov] < 0 and H < H1 and H1 > H2. StartOfUpTrend if C >= simpleavg(C,18) and [DirMov] >= 0 and L > L1 and L1 < L2. GreenTrend if C >= simpleavg(C,18) and [DirMov] >= 0. RedTrend if C < simpleavg(C,18) and [DirMov] < 0.

Code for the author’s color study is set up in the AIQ EDS code file. Figure 7 shows the color studies set up in the charts module. Figure 8 shows the color studies on a chart of Apple, Inc. (AAPL). The black bars are potential entry points in the downtrend.

FIGURE 7: AIQ. The color bar setup in the charts module is demonstrated.

FIGURE 8: AIQ. This shows an example of the color studies applied to a chart of Apple, Inc. (AAPL) with a DMI histogram and an 18-bar simple moving average.

It’s been a challenging market this year, and making trading decisions has never been easy. Which direction the market is likely to move plays a huge part in stock trading decisions.

The Expert Rating system on the market with its combination of 400 rules on the Dow 30 index and the NYSE internals has always provided us an early indication of direction changes.

No system is infallible, and when the Expert System on the market was created, we noticed that ratings of 95 or higher to the upside or downside (maximum rating is 100 btw) were significant. We also noticed a marked improvement in the ratings accuracy if we used a confirmation technique with a a momentum indicator.

After much research we discovered that the Phase Indicator (a version of an MACD histogram) was the most accurate tool to confirm high ratings.

Here’s how we use Phase to confirm a high Expert Rating.

When a rating of 95 up or 95 down is triggered on the market, we look for the Phase histogram to change direction. The change in direction must be to the direction of the rating. This change does not have to happen on the day of the rating, but it must occur within 2 to 3 days either side of the rating day.

If the Phase does not change direction, the rating is considered not confirmed.

This short video analysis of the last 4 ratings shows this process in action.