The Dow fell 128 points, closing at 17,849. The Dow got a low as 17,822, only 22 points from my critical support level of 17,800.

So the Dow is still in No Man’s Land. And because of this, I want to talk about something else this weekend. I want to talk about the importance of having a well thought out strategy.

Most of you know that I’m not a big fan of the commentators or guests on CNBC. I believe that they give you way too much sizzle and not enough steak. As entertainers, they always have one guy saying something, only to have the next guest saying just the opposite. The pattern for the show creates confusion, which is something I don’t need when I’m trying to find a stock to trade. No, I don’t need one guy telling me the stock is a great only to have the next guy telling me to sell it. Besides, they almost never tell why they believe a stock is either good or bad. They just offer their opinion. What good is that?

But I have to tell you that even though I don’t have a lot of positive things to say about the commentators on CNBC, I do like the new app they developed for my iPhone. It’s a terrific and convenient way to get financial news and updated stock quotes. It’s always in my pocket so I can tell what my stocks are doing.

I recently noticed that a new feature has been added to the app called ‘Pro’. I think you might need to subscribe to get some of the information provided by the app, but I did notice that a feature called ‘Squawk Box Portfolio was free. Hmmm? I got curious and decided to investigate its performance.

Well it turns out that the ‘Squawk Box Portfolio’ was actually the picks of 14 different commentators, including two Big Names. Of the 14 stock pickers, there were 8 winners and 5 were losers. The average gain was 5.12 percent. However if you threw out the top two pickers which had gains over 20 percent, the average gain for the rest of the field was only 1.32 percent. And the odds of getting a positive return were only slightly higher than 50-50.

Anyhow, after looking at the results, I decided to look deeper into the portfolios of the two pickers with gains of 20+ percent. I wondered which stocks they picked. Well, as things turned out, I was not surprised. These two pickers had stocks like NFLX, GILD, and APPL in their portfolio. Hmmm? The names sounded familiar. Where have I seen these stocks before?

Of course! All of them had been ranked high on the Member’s Watch List (MWL) during the past few months. NFLX started to move back onto the List in early April. It has remained near the top of the List. Emeritus highlighted the stock for the Honor Roll on 13 April at 474.68. On Friday, NFLX closed at 633.22 for a 33 percent gain! So if you stayed in the stocks on the MWL, you likely beat the pants off of all of the CNBC commentators. Go take a look.

Back in late March – early April, when I was looking to trade energy, stocks like NBR, CLR, CJES, PBR, and ATW were consistently near the top of the MWL. On 6 April, beaten down PetroBras (PBR) was ranked #2 behind ALTR which was on a tear of its own. At the time, PRB was trading at 6.8. It rose to 9.71 over the next month for a 42 percent gain!

But let’s suppose it was 9 April, and you thought you missed the move in energy. On that date, C&J Energy Services (CJES) moved into the top spot on the MWL. It was trading at 13.4. A month later it was trading at 17.3 for a gain of 29 percent! No, you wouldn’t have missed the energy train. You didn’t need to follow the Pros on CNBC. I didn’t see too many energy stocks in their portfolios. If you wanted winners, all you needed to do was be in the top stocks on the MWL.

BTW, whenever I see DIG on the List, I like to trade the energy rabbits…the energy stocks ranked high on the MWL. Remember, most ETFs contain a lot of junk along with a few good performers. So I look for times when one of my sector ‘Sticks in the Sand’, like DIG, is on the List and then trade the individual stocks in that sector from the MWL. This keeps me in the rabbits when the environment is favorable.

So this weekend, while the market is still in No Man’s Land and testing the low of its range, I want you to think more about your long term strategy than what the market is currently doing. Sometimes with all of the hype on CNBC, we tend to get caught up in the events of the day, worrying about what will happen in Greece, or the Jobs Report or what Janet Yellen and the Fed are going to do about interest rates. None of this matters! It’s all fluff and filler in the grand scheme of things. There will always be things in the news to worry about. But these things should NEVER effect your trading decisions.

If you were worried about interest rates, you would NEVER be trading Bonds. So you probably did not noticed when TBT replaced TMF on the Dean’s List and missed its recent move from 43 to 50. BTW, this simple switching strategy has trounced 12 of 14 the stock pickers on CNBC. The model is on track for yet another 50 percent yearly gain.

Here’s what matters: Have a strategy and follow it. When a stock or ETF is ranked high on one of my Lists, it’s ranked high for a reason. It’s very STRONG! So then look at its pattern. Do you see a Hockey Stick? For example, in late April, when TBT moved onto the Dean’s List, it had a nice Hockey Stick Pattern with NARROW Bands. Then when the ETF turned GREEN on 23 April, it was off to the races.

Same for most of the energy stocks in late March. They all had nice HS Patterns with narrow Bollinger bands. As as we learrned from ‘Squeezing the Toothpaste’ , narrow Bollinger Bands are a sign that a Big Move is coming.

So the next time you look at one of the stocks or ETFs on one of the Lists, look for the NARROW Bands. This is especially true if the historical seasonality trends suggest that a Big Move is coming.

If you have a strategy and stick to it, you won’t have to rely on the opinions of other people. You will learn to ignore the fluff from the commentators on CNBC and focus on what matters.

This weekend, take some take some time to go back and look at the performance of the top stocks on the MWL. All of the market leaders were there. Then take some time to think about the strategy you plan to use to be in them going forward. Will it be a rotation strategy, replacing the top stocks whenever they fall off the List? Or will you use my ‘Sticks in the Sand’ approach to trade energy depending on whether DIG or DUG is on the Dean’s List. This is what we did in March. When DIG moved onto the Dean’s List, it was time to look for energy stocks to trade form the Member’s Watch List.

Or will you use the ‘Sticks in the Sand” to trade Bonds, the Dollar or Gold?

This is what matters! And as I’ve pointed out above, listening to the opinions of the commentators on CNBC gets you a 1.32 percent return. It also causes you to be concerned about a lot of things that have nothing to do with making money.

So this weekend, I want you to focus on your strategy. If you don’t have one, and you continue to flip-flop from one strategy to another, and continue to miss big moves, maybe you should think about what you’re doing. Even if you just want to pick stocks to trade, maybe you say to yourself that you’re only going to trade top stocks from the MWL or the Honor Roll whenever The Tide is positive.

But whatever your strategy is, write it down. Post it near your computer. Know all of the conditions of the strategy that need to line up before you decide to enter a trade. Then after you make several trades, evaluate your performance. Be honest with yourself. Did you make or lose money? Did you follow your own rules? Was your strategy too hard or complicated to follow?

Because I believe we’re going to see a lot of volatility in the markets during the next few months, it will be extremely important to have your strategy in place BEFORE things start to become hectic. If the market starts to rally back to 18,350+ and sets up the Major decline I expect, the folks on CNBC will NOT protect you. The time for developing and reviewing your strategy is NOW. Not when the market is testing 18,350 or below 17,800. Now!

You don’t want to be thinking about your strategy once the battle starts. Know what you’re going to do before the panic starts to develop. In the weeks ahead, start testing your strategy. Get comfortable with it. Then believe in it. You’re gonna need it.

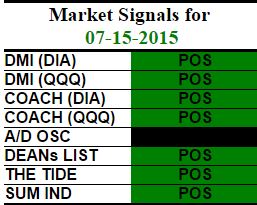

BTW, there was another small change in the A-D oscillator on Friday. So we need to be on the lookout for another Big Move within the next 1-2 days. Now that the Dow is near the 17,800 support level I have been talking about for weeks, if it starts to break down the move could be violent. On the other hand, the market is very oversold now, so it’s possible that Friday’s decline was the end of wave ‘b’ of the a-b-c pattern. So let the market tell you what to do on Monday. If it starts to move higher, it would tell me that 17,800 is holding and a move back to 18,350+ is likely. On the other hand, IF 17,800 does not hold, I’m gonna get short real quick.

Have a great weekend.

That’s what I’m doing,

h

Market Signals for

06-08-2015 |

| DMI (DIA) |

NEG |

| DMI (QQQ) |

NEG |

| COACH (DIA) |

NEG |

| COACH (QQQ) |

NEG |

| A/D OSC |

SM CHG |

| DEANs LIST |

NEU |

| THE TIDE |

NEG |

| SUM IND |

NEG |

All of the commentary expressed in this site and any attachments are opinions of the author, subject to change, and provided for educational purposes only. Nothing in this commentary or any attachments should be considered as trading advice. Trading any financial instrument is RISKY and may result in loss of capital including loss of principal. Past performance is not indicative of future results. Always understand the RISK before you trade.