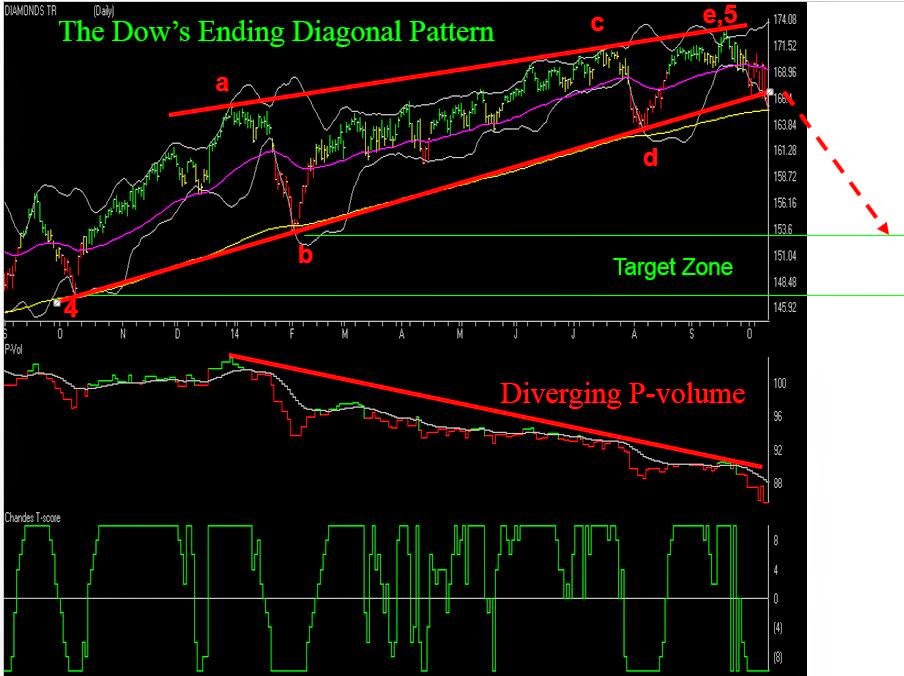

Seems like I have used this title before. That’s probably because I have. It’s also because every once in awhile I lift my head up from “crunching numbers” – in pursuit of that “one great market timing method” – and remember that there really is no such thing and that having a general sense of the overall trend of the markets and adding a touch of common sense can get you pretty far as an investor and trader.

Of course, that’s been easier said than done of late. At times its seems that common sense would dictate doning a Hazmat suit and curling up in the fetal position in a corner until – you know, whatever – passes. With an election coming up we have been informed by both sides that if the other side wins then that will pretty much be the end of humanity as we know it. Which leaves us exactly where? But I need to watch my blood pressure so I will steer clear of politics.

My Writing (or Lack Thereof) of Late

I have been writing very little of late. The good news for me is that JayOnTheMarkets.com is not a paid site and there are no deadlines and no one is waiting for me to tell them what to do next in the markets. Which is probably a good thing since the truth is that I have never been more unsure of exactly what the h?$% is going on in the markets (or the world around us, come to think of it) than I have been of late. Hence the lack of more frequent updates. As the saying goes, “If you don’t have something intelligent to say, don’t…” – well come to think of it I have never really adhered to that rule in the past. Never to late to start, I guess. In any event, thank goodness I am a systematic trader.

In trying to make sense of things, on one hand a perusal of the evidence in recent months led me to think that a major top was forming. On the other hand, the trend (except for a recent short-lived dip by some of the major averages below their 200-day moving averages) has remained “up” and we are now in what has historically been a very bullish seasonal period (also the standard most bullish 6 months of the year starts on November 1st).

So the bottom line is that if you want to be bullish you can make a pretty good case. On the other hand, if you want to be bearish you can also make a pretty good case.

What’s a guy or gal to do?

Well hopefully your answer is the same as mine: Continue to follow your objective, well thought out trading plan – one that incorporates some risk controls in case things don’t go the way you planned.

Sounds so simply when its put that way, doesn’t it? Towards that end, let me offer a simple “Non Rocket Science” method for identifying the long-term trend of the stock market.

Jay’s Non-Rocket Science Stock Market Trend Identification Method (JTIM)

Notice that this ridiculously long title (hence JTIM for short) includes the phrase “Trend Identification” and not the phrase “Market Timing”. If I were truly interested in full disclosure the title would actually be something like “Jay’s Non-Rocket Science Let’s Not Ride the Bear Market All the Way to the Bottom for Crying Out Loud” Method. But that one was really long winded.

The purpose of this method is simply this, nothing more, nothing less: to avoid riding an extended bear market all the way to the bottom all the while hoping that one day it will bounce back. When this method gives a sell signal it simply means that it “may be” time to play defense. That might mean selling a few stock market related holdings, that might mean selling everything related to the stock market, or it might mean hedging and existing portfolio.

It also means that there is a chance that you may take defensive action and later end up wishing that you had not. Sorry folks, that just kind of the nature of trend following. But one thing I have learned since, well, the time I had a lot of hair until now, is that selling now and buying back in at a slightly higher price is typically preferable to riding a 20%, 30% or 40% or more drawdown.

Now some people may respectfully disagree with that opinion. But these types of drawdowns can scar an investor’s psyche – and adversely affect their judgment in the future – for a long time – even after their portfolio eventually bounces back. In addition, riding a massive drawdown like DiCaprio and Winslet riding the final plunge of the Titanic opens an investor to one of the most devastating mistakes of all – i.e., selling at or near the bottom (Though fortunately not to hypothermia like DiCaprio – and just for the record, seriously, couldn’t Winslet have just schooched over a little bit and made enough room for both on that door or whatever it was she was floating on? But I digress).

This reminds me to remind you of:

Jay’s Trading Maxim #78: Drawdowns make people act stupid (the more the drawdown, the more the stupid).

So here are the (granted, imperfect) JTIM rules:

*If the S&P 500 Index closes for two consecutive months below its 21-month moving average AND also closes below its 10-month moving average, the trend is deemed “Bearish”.

*While the trend is deemed “Bearish”, if the SPX 500 Index closes one month above its 10-month moving average then the trend is deemed “Bullish.”

That’s it.

JTIM Results

The results must be measured based on what the method is trying to achieve – i.e., avoiding massive, long term drawdowns – so as to avoid “acting stupid” (and to avoid ending up like DiCaprio, but I repeat myself). Over the course of time the results look pretty good. Of course, it also depends to some extent on how you define “good”, because from time to time – and over certain extended periods of time between the beginning and end – the results don’t look so good. Allow me to explain.

In general terms, it goes like this:

Good: This method avoided most of the 1973-1974 bear market.

Not So Good: Between 1977 and 1991 there were 5 “sell” signals. In all 5 cases an investor who “sold everything” based on these signals would have bought back in at a higher price. An investor would have missed drawdowns of -9.6% in 1977-78 and -12.7% in 1981-82. But all other sell signals during the great bull market of the 80’s and 90’s witnessed drawdowns of no more than -4.0%.

Good: The last three sell signals (2000, 2002, and 2008) were followed by drawdowns of -28%, -29% and -50%, respectively.

Figure 1 displays the results in tabular form:

Figure 1 – Jay’s Trend Identification Method Signals

The key thing to note is that over the past 40+ years this method outperformed buy-and-hold (by almost 2-to-1 if interest earned while out of the market is added in; See Figure 6).

Figures 2 through 5 display the signals on SPX monthly bar charts.

Figure 2 – SPX with JTIM Signals 1970-1984 (Courtesy: AIQ TradingExpert)

Figure 3 – SPX with JTIM Signals 1984-1994 (Courtesy: AIQ TradingExpert)

Figure 4 – SPX with JTIM Signals 1994-2004 (Courtesy: AIQ TradingExpert)

Figure 5 – SPX with JTIM Signals 2004-2014 (Courtesy: AIQ TradingExpert)

Figure 6 displays the growth of $1,000 using JTIM (adding 1% of interest per year while out of the market) versus buy-and-hold since 1970.

Figure 6 – Growth of $1,000 using JTIM (blue line) versus buy-and-hold (red line) since 1970

And just to complete the picture Figure 7 displays the growth of $1,000 invested in SPX only when the system is bearish.

Figure 7 – Growth of $1,000 when JTIM is bearish (1970-present)

For the record, had an investor bought an held the S&P 500 only during those period when JITM was bearish since 1970, an intitial $1,000 investment would now be worth only $540 (i.e., a loss of -46%). Or as we “professional market analysts” refer to it – Not So Good.

Summary

So is this the “be all, end all” of market timing? Clearly not. During most of the 80′s and 90′s, getting out of the market for any length of time typically cost you money. Still, since nothing of the “be all, end all” variety actually exists some investors may find it useful to note the status of this simple model, at the very least as an alert that:

a) a lot of bad news can typically be ignored if the model says the trend is “up”, and,

b) some defensive action may be wise if the model says the trend is “down.”

Alright, excuse me, I have to get back into my Hazmat suit.

Jay Kaeppel

Chief Market Analyst at JayOnTheMarkets.com and AIQ TradingExpert Pro (http://www.aiq.com) client

http://jayonthemarkets.com/

Jay has published four books on futures, option and stock trading. He was Head Trader for a CTA from 1995 through 2003. As a computer programmer, he co-developed trading software that was voted “Best Option Trading System” six consecutive years by readers of Technical Analysis of Stocks and Commodities magazine. A featured speaker and instructor at live and on-line trading seminars, he has authored over 30 articles in Technical Analysis of Stocks and Commodities magazine, Active Trader magazine, Futures & Options magazine and on-line at www.Investopedia.com.